How Website Behaviour Revealed EV Demand Before the Showroom Did

By Sam Benbow, Head of Growth & Automotive Specialist at Force24

This article explores the relationship between rising fuel prices and EV research behaviour. I won’t be getting into foreign affairs, why this has all happened and what comes next, so I can promise we won’t go that deep! Most interestingly, I’ll be discussing how early intent signals can be spotted before they translate into enquiries, giving marketing and sales teams first-mover advantage.

The theme of this article stemmed from a recent meeting we had with a dealership. Simply out of topical interest, we’d asked if they’d seen an increase in EV enquiries following the loathed recent spike in petrol and diesel prices, but nothing had been flagged at showroom level. When we then brought up the same dealership’s identified traffic volumes for 2026 YTD, a different picture emerged. There had been a clear and patterned month-on-month increase in EV and hybrid browsing activity. This hadn’t been noticed yet, which is understandable as this isn’t something most teams have the privelege of time to track or report on manually.

The obvious question to us was then whether it was just them, or in fact a wider industry trend. So we got back to the office and investigated. We measured the same data points across all our automotive customers with EV and Hybrid offerings to see if the pattern held. What came back was pretty clear – showing this in fact not to be an anomaly, but happening across the market. The findings will be discussed throughout this article.

What the data is telling us

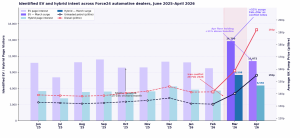

To better understand what was happening, I looked at identified browsing behaviour across our automotive customers. Each visit can be linked back to a known individual, connected to a contact record, and built out with things like vehicle history and previous engagement. When you plot that against UK pump prices over the eleven months from June 2025 to April 2026, a clear pattern starts to emerge. It is one of the more noticeable shifts in buyer behaviour we have seen across the network.

Identified EV and hybrid page visitors across Force24 automotive dealer customers vs. UK average pump prices, June 2025 to April 2026.

When you look at the data over time, the pattern is fairly clear. From July 2025 through to February 2026, combined EV and hybrid browsing held in a steady range, roughly 15,000 to 17,000 identified visitors each month, while fuel prices stayed relatively flat at around £1.32 to £1.36 for petrol and £1.38 to £1.43p for diesel. That gives you a good baseline of how many people are already considering a switch, even when conditions are stable.

Then things started to move. Towards the end of February,as well all know (unless you’re an EV driver) ‘wider global events’ began to push fuel prices up, with diesel rising by around 17 pence per litre within a few weeks and petrol following behind. What stood out was how quickly buyer behaviour responded to this. From February to March, identified EV and hybrid browsing increased by 52%, reaching 23,298 visitors, the highest point in the dataset.

What is more interesting is what happened next. April did not drop back to previous levels. Even with diesel at £1.92 and petrol at £1.55, browsing activity held at 17,622 visitors, around 11% above the earlier baseline. That suggests this was not just a short-term spike, but a shift in how buyers are feeling about the short-medium term.

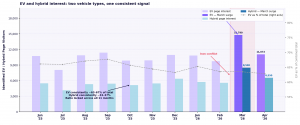

Within that, there is also another consistent pattern: The split between EV and hybrid interest stays almost unchanged at around 63:37 across every month, before, during and after the increase. So this is not just a move towards EVs specifically. It points more towards a broader reconsideration of powertrain, with buyers actively exploring both options as running costs change.

EV vs hybrid page interest, June 2025 to April 2026. Both vehicle types move in lockstep throughout, with the EV-to-hybrid ratio holding steady at approximately 63:37.

The February-to-March increase does not look like a short-term reaction to the news cycle. April suggests something more sustained, with many of those buyers still actively researching.

Why flagging this insight on an ongoing basis is commercially valuable

In large, every UK dealership faces the same challenge. By the time a buyer walks into a showroom, most of the hard work has probably already happened. They’ve done the research, weighed up their options, and are well on their way to making a decision. The dealerships who got in front of them earlier in that decision making process are usually the ones in the strongest position to get the sale.

That is why the earlier window of the cycle matters so much. The four to twelve weeks between someone first starting to think differently about their next car and actually stepping onto a forecourt is where we see buying decisions really beginning to take shape. It is also the part of the journey that has traditionally been hardest to see clearly. That is now starting to change as we receive more data and signals to interpret. This is where those early buyer signals become useful. When you can see who is actively researching, link that activity to real people, and connect them to the right vehicle, you are in a much stronger position to capture demand as it builds rather than reacting once it is already visible.

As mentioned earlier, we see the typical consideration-to-showroom cycle in automotive usually sitting somewhere between four and twelve weeks. So the people we are seeing showing EV and hybrid interest are not future buyers in some distant sense. Rather they are likely to become the next wave of enquiries and test drives. They are already in the funnel, already doing their research, and almost most importantly, already reachable.

The dealerships who engage them at this stage tend to be the ones in a much stronger position when it comes to conversion. This is where the commercial value of forward-looking insight really comes in. From what I have seen, most of the market is still working off two types of demand signals.

- What has already happened; Enquiries, test drives, registrations. These are useful, but by the time those numbers start to move, a lot of the outcome is already taking shape.

- What is happening right now; People actively research, comparing options, and forming a view before they ever make contact. That is the part we can now see more clearly.

When brands work from this first (which is common), they are always reacting. This looks like responding to the enquiries that come in and engaging the people who have already raised their hand. This is a good start, but it does mean competing at the same point as everyone else, which will bring down your enquiry-conversion rate. If you are working with earlier signals, this changes the dynamic. Now, you can instead start to engage people while they are still figuring things out, while preferences are still forming, and while there is more space to be relevant. That is usually where the advantage sits as you will be a frontrunner in the buying decision.

That is all about spotting trends before they emerge, which leads nicely back onto a quick recap our findings.

The numbers, summarised

To recap, looking across the full dataset, a few things stand out quite clearly

+52%

February to March increase in identified EV/hybrid intent across all dealers in the network

23,298

Named individuals showing EV or hybrid intent in March 2026

17,622

Identified prospects in April 2026 already, holding 11% above the pre-March baseline

63:37

Consistent EV-to-hybrid ratio across all 11 months, pointing to broad powertrain reconsideration

Looking a bit closer at the shift

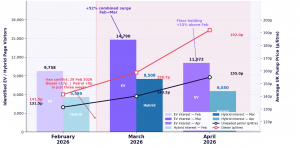

When you break the data down at dealer level, the pattern becomes more consistent. Every dealership in the network saw an increase from February into March, rather than this being driven by a small number of outliers.

What is also interesting is that, for some dealers, April has already gone on to exceed their March figures. That suggests this is not just a short-term spike, but something that is continuing to play out. Taken together, it points to a broader shift across the market, rather than something isolated to a particular group or location.

February, March and April 2026 identified EV and hybrid visits vs. UK pump prices.

Making action from this insight with contact-by-contact intelligence

Seeing what is happening early is one thing, but being able to actually do something with it is the important bit. ”Bring me solutions not problems!”

The challenge is usually where your marketing team is then tasked with turning that insight into action at the level of the individual. What has changed that can help with this is the ability to connect that behaviour back to a real person in the database, with context around their current vehicle, finance position, service history and recent engagement.

From there, it becomes much more practical. Instead of treating everyone the same, you can start to work out what is most relevant for that individual at that point in time, and respond accordingly. That might be the right vehicle, the right message, or simply the right moment to reach out.

How to turn early signals into something you can actually act on

In practice, this usually comes down to a few simple things done well. At Force24, our team does this for dealerships through our automated data matching feature, Nexus. For them, this means ultimate relevancy benefits covering the below four areas:

- Understand where someone is in their journey

Looking at a person’s current vehicle, their service history, finance position and what they have been browsing recently starts to give a pretty clear picture of where they are. Someone casually looking is very different to someone comparing specific models or returning multiple times. - Match them to something relevant

Once you have that context, it is less about pushing the most popular EV or hybrid and more about finding what actually fits. That might be based on what they drive today, what price range they are leaning towards, or the types of vehicles they have been looking at. - Respond in a way that feels timely

Rather than building broad campaigns, it becomes more about responding to what that individual is doing. That could be a relevant vehicle, a cost comparison, or a well-timed nudge to take the next step. The key is that it lines up with their behaviour, not your send calendar. - Do it consistently across the database

The real shift is being able to do this across thousands of contacts, not just a handful. So instead of manually building lists and campaigns, you have a more consistent way of responding to people as their behaviour changes.

What this means for dealerships

This is something that is becoming more noticeable across the dealerships we speak to. There definitely appears to be a shift in the way people are buying cars. More of the journey is happening online, more of the research is happening earlier, and decisions are being shaped by things like fuel prices, tax changes and general market conditions in a way that feels more immediate and responsive than it used to.

At the same time, the number of people actively in-market at any one time has not really changed, which means dealers are still competing for that same pool of buyers – now often with tighter margins, which puts more pressure on how and when those buyers are engaged.

What we are now hearing in our conversations is that the few dealerships performing better are not necessarily doing anything radically different, but they are a bit closer to what is actually happening day to day and they have a clearer view of who is where in their own lifecycle. That usually means having enough context around each buyer to make communication feel more relevant to what they are actually looking at, rather than relying on broader campaigns. It also means having a way of doing that consistently, without it becoming a manual task every time someone’s behaviour changes.

It is less about a complete shift in strategy and more about tightening the connection between what you can see and what you do next. The advantage tends to come from spotting things a little earlier, responding in a way that feels more appropriate, and being able to do that consistently across the database.

The opportunity is there now

With diesel sitting at £1.92 per litre and petrol at £1.55, the conditions that have been driving interest in EVs and hybrids have not really eased. The data suggests that the higher level of research activity is holding, rather than dropping back, and the people who started looking earlier are still actively comparing options. At the same time, new buyers are beginning that journey each week.

This likely means the people currently showing interest are likely to become the next wave of enquiries and test drives and are currently already in the research phase, already exploring options, and already reachable if you know where to look.

I hope you enjoyed this article and found it useful. If it’s sparked any questions or made you think differently about what might already be sitting in your own data, feel free to reach out to me personally. I’m always happy to take a look and help you uncover the early intent signals that could be there in your own data ready to act on.

Back to FWD: ThinkingGet in touch

Give us a shout.

Ready to take your marketing up a gear? Give us a call or drop us an email – our UK-based team is on hand to help.

Talk to us